Featured

Table of Contents

Insurance provider will not pay a minor. Instead, consider leaving the money to an estate or depend on. For more in-depth details on life insurance coverage get a copy of the NAIC Life Insurance Policy Purchasers Guide.

The IRS positions a limit on exactly how much cash can go into life insurance policy costs for the plan and just how promptly such premiums can be paid in order for the plan to retain all of its tax advantages. If specific limitations are exceeded, a MEC results. MEC policyholders might be subject to tax obligations on circulations on an income-first basis, that is, to the level there is gain in their plans, along with fines on any kind of taxable quantity if they are not age 59 1/2 or older.

Please note that impressive loans accrue interest. Earnings tax-free treatment likewise assumes the car loan will eventually be satisfied from income tax-free survivor benefit earnings. Car loans and withdrawals minimize the plan's cash worth and survivor benefit, might trigger certain policy advantages or bikers to become not available and may raise the opportunity the plan might gap.

4 This is offered via a Long-term Treatment Servicessm motorcyclist, which is readily available for an added fee. Additionally, there are limitations and limitations. A client might get approved for the life insurance policy, but not the biker. It is paid as a velocity of the survivor benefit. A variable universal life insurance policy contract is an agreement with the key objective of giving a fatality advantage.

How do I get Mortgage Protection?

These portfolios are carefully handled in order to please stated financial investment objectives. There are costs and charges connected with variable life insurance agreements, including mortality and risk costs, a front-end tons, administrative costs, investment administration fees, abandonment costs and costs for optional cyclists. Equitable Financial and its associates do not supply lawful or tax advice.

And that's wonderful, since that's precisely what the fatality advantage is for.

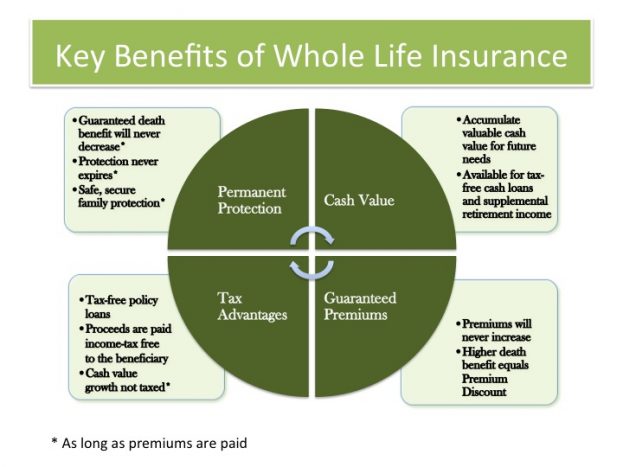

What are the benefits of whole life insurance? Right here are a few of the key points you need to know. One of one of the most appealing benefits of buying an entire life insurance policy is this: As long as you pay your costs, your survivor benefit will certainly never ever expire. It is ensured to be paid no matter of when you die, whether that's tomorrow, in five years, 80 years and even further away. Term life.

Assume you don't require life insurance coverage if you do not have kids? There are numerous benefits to having life insurance policy, also if you're not sustaining a family members.

How can I secure Income Protection quickly?

Funeral expenditures, funeral costs and medical expenses can include up (Final expense). The last thing you desire is for your enjoyed ones to shoulder this added concern. Long-term life insurance policy is readily available in various amounts, so you can choose a fatality benefit that fulfills your needs. Alright, this just uses if you have kids.

Identify whether term or permanent life insurance policy is right for you. As your individual circumstances modification (i.e., marital relationship, birth of a youngster or job promotion), so will certainly your life insurance policy needs.

Generally, there are two kinds of life insurance policy plans - either term or irreversible strategies or some mix of the 2. Life insurance providers provide various forms of term plans and traditional life policies as well as "interest delicate" products which have actually come to be extra prevalent because the 1980's.

Term insurance coverage offers protection for a given amount of time. This duration could be as brief as one year or provide coverage for a certain variety of years such as 5, 10, two decades or to a defined age such as 80 or in many cases approximately the earliest age in the life insurance mortality.

What is a simple explanation of Final Expense?

Presently term insurance coverage prices are really competitive and amongst the most affordable historically knowledgeable. It must be noted that it is a widely held idea that term insurance is the least expensive pure life insurance protection readily available. One needs to examine the policy terms carefully to choose which term life alternatives appropriate to satisfy your certain situations.

With each new term the costs is boosted. The right to restore the plan without proof of insurability is a crucial advantage to you. Or else, the danger you take is that your health and wellness may deteriorate and you might be incapable to get a policy at the same rates or even whatsoever, leaving you and your recipients without protection.

The length of the conversion duration will differ depending on the kind of term plan acquired. The premium rate you pay on conversion is typically based on your "current obtained age", which is your age on the conversion date.

Under a degree term plan the face quantity of the policy continues to be the very same for the entire period. With lowering term the face quantity lowers over the period. The premium stays the very same every year. Often such policies are sold as home loan security with the amount of insurance coverage lowering as the balance of the home loan decreases.

What happens if I don’t have Guaranteed Benefits?

Commonly, insurance companies have actually not can change costs after the plan is sold. Because such policies might continue for several years, insurance firms must make use of conventional mortality, passion and cost rate price quotes in the premium computation. Adjustable costs insurance policy, nonetheless, permits insurers to offer insurance coverage at reduced "current" premiums based upon much less conservative presumptions with the right to change these costs in the future.

While term insurance coverage is developed to provide protection for a defined amount of time, long-term insurance is designed to give insurance coverage for your entire lifetime. To maintain the premium price level, the costs at the younger ages surpasses the actual cost of security. This added costs develops a book (cash money value) which aids spend for the policy in later years as the expense of defense increases over the premium.

The insurance firm invests the excess premium bucks This type of plan, which is occasionally called cash money worth life insurance, creates a financial savings aspect. Cash worths are vital to an irreversible life insurance coverage policy.

{kind=link}

Latest Posts

How can Level Term Life Insurance Quotes protect my family?

Death Benefits

What Is Level Term Life Insurance? A Complete Guide